Imagine this: Your company needs new office laptops. You tell your supplier, but something gets lost in translation—wrong models, incorrect quantities, or unexpected charges. Sound familiar? This is where a purchase order (PO) comes in.

A purchase order is like a restaurant order slip—it tells the supplier exactly what you want, at what price, and by when. It’s a legally binding document that protects both the buyer and the supplier.

For finance teams, AP departments, controllers, and CFOs, POs are more than just paperwork. They help track expenses, prevent unauthorized purchases, and keep audits stress-free. Let’s break it down step by step.

What is a Purchase Order?

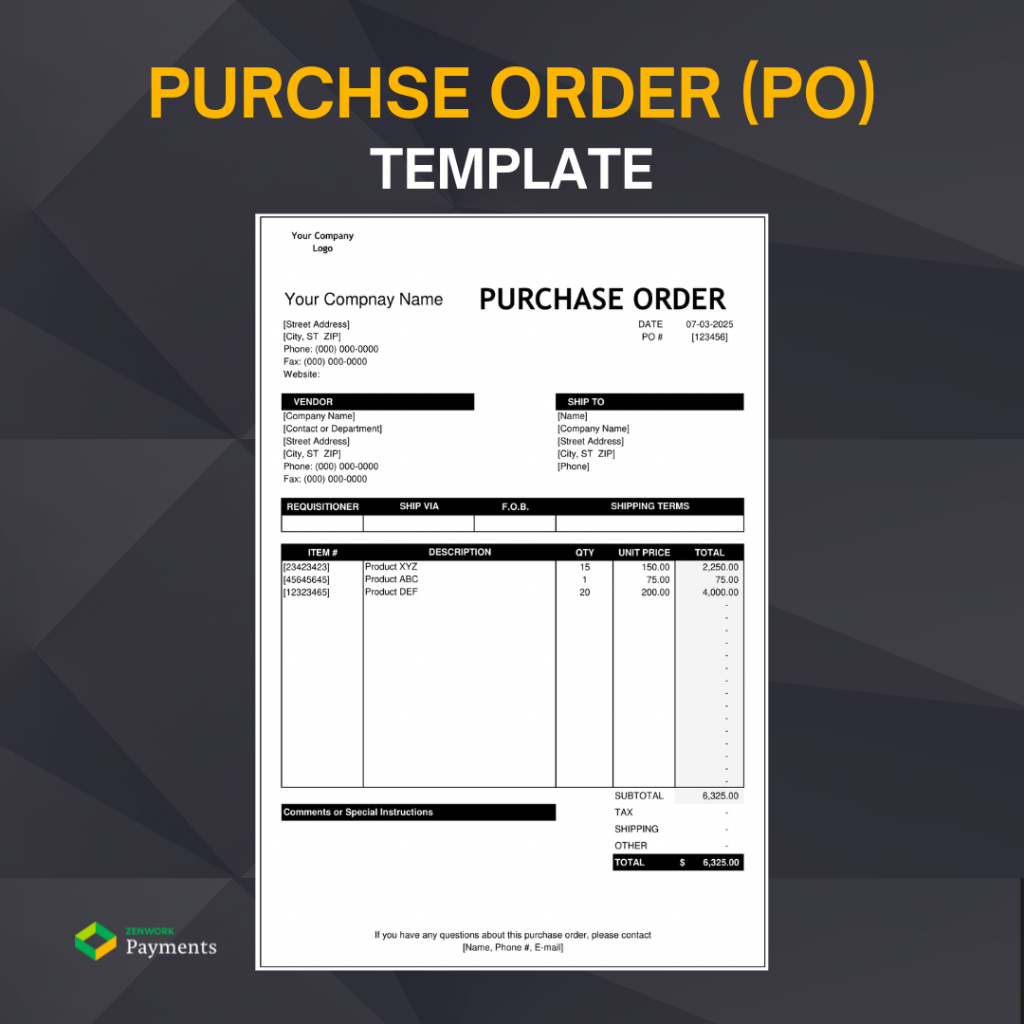

A purchase order (PO) is a document a buyer sends to a supplier to request goods or services. It outlines:

- Product/service details

- Quantity

- Price

- Delivery date

- Payment terms

Once accepted by the supplier, it becomes a legally binding contract.

Download: Purchase Order Template

A Quick History of Purchase Order

Before automation, businesses relied on handwritten or printed POs, leading to lost paperwork and approval bottlenecks. Today, 80% of businesses use digital procurement systems to streamline the PO process.

The Main Purpose and Benefits of Purchase Orders

Why bother with POs? Here’s what they help with:

- Legal protection – Avoid disputes with clear, documented agreements.

- Budget control – Track spending and prevent overspending.

- Inventory management – Order what’s needed, when it’s needed.

- Audit trail – Keep records for tax season and financial audits.

- Prevention of duplicate or unauthorized purchases – No surprise expenses.

- Smoother vendor relationships – Suppliers appreciate clear instructions.

How Does a Purchase Order Process Work?

The PO process isn’t as complicated as it sounds. Here’s a step-by-step breakdown:

- Purchase Requisition – Employee requests a purchase internally.

- PO Creation & Approval – AP or procurement drafts the PO and gets it approved.

- Sending PO to Vendor – Supplier receives and confirms the order.

- Goods/Services Received – The company checks if the order is correct.

- Invoice Received & Matched – Three-way matching ensures the invoice, PO, and receipt align.

- Payment Processing – AP team processes the payment.

- PO Closure & Record Keeping – The PO is closed, and data is stored for audits.

Different Types of Purchase Orders

- Standard Purchase Orders (SPO)

- Blanket Purchase Orders (BPO)

- Planned Purchase Orders (PPO)

- Contract Purchase Orders (CPO)

- Digital Purchase Orders (DPO)

Not all POs are created equal. Businesses use different types depending on the situation:

-

Standard Purchase Orders (SPO)

- Used for one-time purchases

- Example: Buying 10 office chairs from a supplier

-

Blanket Purchase Orders (BPO)

- Used for recurring orders over time

- Example: Ordering printer paper every month at a fixed rate

-

Planned Purchase Orders (PPO)

- Used for scheduled purchases with estimated delivery dates

- Example: Buying raw materials for quarterly production

-

Contract Purchase Orders (CPO)

- Used when long-term agreements are needed but quantities and delivery dates vary

- Example: Partnering with a vendor for on-demand IT support

-

Digital Purchase Orders (DPO)

- Used in automated procurement systems

- Example: POs generated and tracked in an AP automation tool

Each type serves a specific need. One company I worked with switched to digital POs and saw a 60% drop-in processing time, making life a lot easier for everyone.

Purchase Order vs. Related Documents

It’s easy to confuse POs with other procurement documents. Here’s how they differ:

PO vs. Invoice

- PO: Buyer’s request to a supplier – A pre-agreement on what will be delivered.

- Invoice: Supplier’s bill to the buyer after fulfilling the order.

PO vs. Sales Order

- PO: Created by the buyer.

- Sales Order: Issued by the seller confirming the PO.

PO vs. Purchase Requisition

- Purchase Requisition: Internal request for approval before creating a PO.

- Purchase Order: Sent to the vendor after approval.

Creating Effective Purchase Orders

When drafting your POs, here are some tips to keep it straightforward:

- Include clear details: What’s being bought, how much, and when.

- Avoid common mistakes: Missing key info or using vague terms.

- Keep terms simple: Use plain language.

- Set approval levels: Know who signs off on what.

- Numbering systems: Help keep things organized.

Purchase Order Templates and Resources

A well-structured PO template saves time. Here’s what to include:

- Company name & contact details

- Supplier name & contact details

- PO number & date

- Itemized list of products/services

- Pricing & payment terms

- Delivery instructions

Check out free PO templates from Smartsheet.

Automating the Purchase Order Process

Is your team still using spreadsheets and emails for POs?

AP automation tools like Zenwork Payments, Tipalti, and Procurify cut down PO processing time by 50-75%.

Signs You Need PO Automation:

- Too many manual approvals causing delays

- Frequent duplicate or lost orders

- Difficulty tracking spending in real-time

Benefits of Automated POs

Automated purchase orders can offer several benefits including:

✅ Faster processing

✅ Fewer errors

✅ Improved compliance

✅ Better spend visibility

✅ Stronger vendor relationships

Common Purchase Order Challenges and Solutions

Every system has hiccups. Here are some common issues and what to do:

- Handling changes: Set up clear procedures for exceptions.

- Incomplete orders: Make sure all required fields are filled out.

- Vendor non-compliance: Build penalties into contracts.

- Approval bottlenecks: Simplify your workflow.

- Global challenges: Use multi-currency and region-specific settings.

A mistake that often happens is rushing the approval process, which leads to costly errors. Slow down, double-check, and keep an eye on the details.

FAQs About Purchase Orders

- When is a purchase order legally binding?

Once both parties sign off, it’s a contract.

- Can purchase orders be modified after approval?

Yes, but changes should be documented and re-approved.

- How long should purchase orders be kept on file?

Typically, for at least 7 years, but check your local regulations.

- Are purchase orders required for all purchases?

Not always—but they help keep things orderly.

- How do purchase orders improve financial control?

By setting clear budgets and tracking spending.

- What are the risks of not using purchase orders?

Duplicate orders, overspending, and a messy audit trail.

Wrapping Up

Purchase orders might seem like just another form to fill out, but they’re a powerful tool to keep your business organized. They not only protect you legally but also make sure your spending aligns with your budget. If you’re looking to make your procurement process smoother, think about investing in a good PO system—digital systems can really transform your workflow.

Before you go, ask yourself: Could my team benefit from a simpler, more transparent ordering process? If the answer is yes, it might be time to take another look at how you manage purchase orders.

Ready to transform your AP process?

Start Your 30-Day Free Trial with Zenwork Payments AP Automation Software and experience the benefits of automated AP processing.